The key to adapting your health insurance isn’t just switching plans; it’s strategically repositioning your medical needs from a « convenience » to a documented « necessity. »

- Insurers use strict definitions of medical necessity to deny claims for items like power chairs. Proactive, quantified documentation is the only way to counter this.

- Lesser-known Special Enrollment Periods (SEPs) triggered by chronic conditions or life changes are your most powerful tools for bypassing annual waiting times.

Recommendation: Stop being a passive policyholder. Start actively managing your coverage by building a medical necessity case file before you need to make a claim.

For seniors managing a chronic condition, a common fear materializes when a familiar health insurance plan suddenly feels inadequate. As mobility decreases or care needs intensify, the coverage that once seemed comprehensive can reveal critical gaps. The standard advice— »review your plan annually » or « call your provider »—often falls short because it’s reactive. It positions you as a supplicant asking for help after a problem has already become urgent.

This approach misunderstands the fundamental dynamic at play. Health insurers operate on a strict set of rules, definitions, and risk calculations. They are not designed to intuitively adapt to your evolving health story. The most common point of failure is the distinction between what they define as a « medical necessity » versus a mere « convenience. » A power wheelchair that enables you to stay in your home might seem essential to you, but to a plan administrator, it could be coded as a convenience if not properly justified.

But what if the key wasn’t to plead your case, but to strategically master the insurer’s own rulebook? This guide reframes the challenge. It’s not about finding a « better » plan; it’s about proactively restructuring your existing situation to make your needs undeniable. It’s about learning to speak the language of medical necessity, identifying hidden enrollment triggers, and unlocking benefits you’re already entitled to but have never used.

This article will provide a strategic roadmap to take control of your health coverage. We will deconstruct why standard policies fail, provide a framework for documenting your needs, and reveal the specific windows of opportunity and financial traps you must be aware of to secure the care you deserve.

Summary: A Strategic Guide to Adjusting Health Insurance for Evolving Needs

- Why Your « Standard » Policy Fails to Cover Advanced Mobility Needs?

- How to Write an Appeal Letter That Reverses a Claim Denial?

- Short-Term vs Long-Term Care Riders: Which Is Essential After 75?

- The Late Enrollment Penalty That Haunts Retirees for Life

- When to Switch Plans: The Enrollment Window You Must Not Miss

- Why Your Insurance Policy Has « Hidden » Prevention Benefits You Never Use?

- How to Document Medical Necessity to Get Insurance to Pay for Power Chairs?

- How to Organize Complex Medical Records for Seniors Without Getting Overwhelmed?

Why Your « Standard » Policy Fails to Cover Advanced Mobility Needs?

The primary reason a « standard » health policy often fails as a chronic condition progresses is its rigid definition of what constitutes a medical necessity versus a convenience. Insurers, particularly Medicare, have established stringent criteria to prevent paying for what they deem to be lifestyle enhancements. This becomes painfully clear when a senior requires an advanced mobility device, such as a power wheelchair. While you see it as essential for maintaining independence at home, the insurer sees a high-cost item that must be rigorously justified.

The default assumption is that a cane or walker should suffice. To get a more advanced device covered, you must build a case that proves all lesser options are insufficient for performing Activities of Daily Living (ADLs) within the home. Coverage for a device used primarily for navigating the outdoors is often denied, as it’s classified as a convenience. This forces seniors and their families into a frustrating cycle of providing evidence that their needs are not just for comfort but for fundamental daily function.

For instance, Medicare’s prior authorization process for power wheelchairs is a prime example of this barrier. It requires extensive documentation, including face-to-face examinations and specialist orders. The system is designed to deny coverage if the device can be framed as being for ‘convenience’ rather than a documented medical need, effectively re-labeling an essential mobility aid as a non-essential luxury. This policy architecture is why your plan seems to fail you right when you need it most—it was not designed for your evolving comfort, but for a fixed, narrow definition of medical necessity.

How to Write an Appeal Letter That Reverses a Claim Denial?

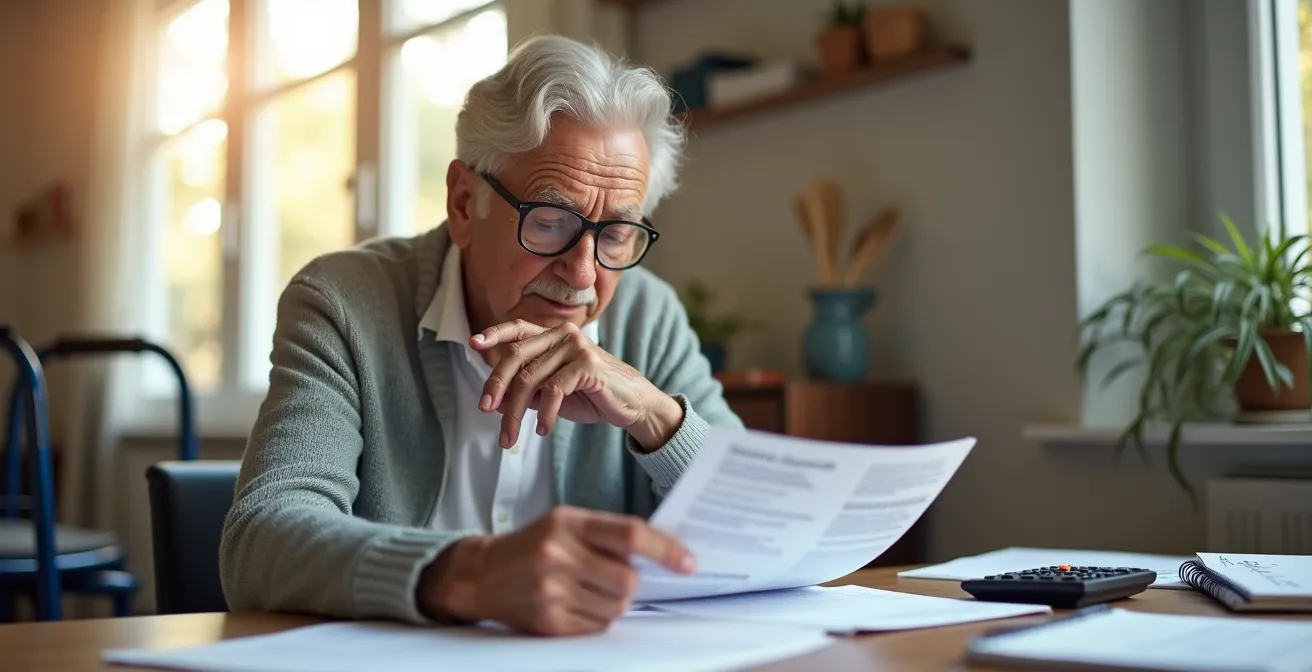

When a claim is denied, the natural response is often emotional—a mix of frustration, fear, and injustice. Many appeal letters are written from this perspective, focusing on personal hardship and the perceived unfairness of the decision. Unfortunately, this is the least effective strategy. An appeal that reverses a denial is not a plea for sympathy; it is a clinical, evidence-based argument that systematically dismantles the insurer’s reason for denial using their own language and standards.

The goal is to transform your appeal from an emotional story into a professional counter-argument. You must address the specific policy clause or justification cited in the denial letter and provide targeted evidence that proves it was misapplied. This requires a shift in mindset: you are no longer a patient but the manager of a case file. Every piece of documentation, every doctor’s note, and every test result becomes a piece of evidence. Organizing these documents systematically is not just for tidiness; it is a strategy to present an overwhelmingly logical and irrefutable case.

As the image above illustrates, a successful appeal is built on order and clarity. A vague complaint is easily dismissed, but a numbered list of enclosed, relevant medical records that directly refutes the insurer’s position is much harder to ignore. The following table breaks down the difference between a weak, emotional plea and a strong, professional appeal structure that is far more likely to succeed.

| Professional Appeal Structure | Emotional Plea (Less Effective) |

|---|---|

| Summary of Condition (factual, medical terminology) | Personal story of suffering |

| Denied Service & Specific Policy Clause Referenced | General complaint about denial |

| Clinical Justification with Medical Evidence | Opinion-based arguments |

| List of Enclosed Evidence (organized, numbered) | Scattered supporting documents |

| Caregiver Impact Statement with Quantified Data | Family testimonials about hardship |

Short-Term vs Long-Term Care Riders: Which Is Essential After 75?

For individuals over 75, the traditional debate between short-term care (STC) and long-term care (LTC) insurance becomes largely academic, as the cost of securing a new LTC policy at this age is often prohibitive. With more than two-thirds of Medicare beneficiaries having multiple chronic conditions, the risk profile makes underwriting incredibly expensive or impossible. This creates an « uninsurability trap » where the people who need care the most are the least able to get coverage. This is where a more strategic approach focusing on hybrid plans becomes essential.

Rather than focusing on traditional riders, the foresight-driven strategy is to explore Medicare Advantage plans known as Chronic Condition Special Needs Plans (C-SNPs). These plans are specifically designed for individuals already diagnosed with severe or disabling chronic conditions like diabetes, heart failure, or dementia. Unlike traditional insurance that you must buy before you get sick, C-SNPs are plans you can often enroll in *because* you are sick, provided you meet the plan’s specific criteria.

A C-SNP represents a modern, integrated approach. For example, many of these plans offer specialized coverage such as $0 copays for chronic condition prescription drugs, access to dedicated care coordinators who help manage your treatment, and condition-specific benefits that are not available in standard plans. Crucially, being diagnosed with a qualifying condition can trigger a Special Enrollment Period, allowing you to switch into a C-SNP outside of the annual enrollment window. For seniors over 75, this shifts the focus from buying expensive, forward-looking LTC riders to leveraging a current diagnosis to enroll in a specialized plan that provides immediate, targeted benefits.

The Late Enrollment Penalty That Haunts Retirees for Life

One of the most dangerous and irreversible traps in Medicare is the Part B Late Enrollment Penalty (LEP). This is not a one-time fee but a permanent surcharge added to your monthly premium for as long as you have Part B. The penalty is calculated as 10% of the standard premium for each full 12-month period you were eligible for Part B but didn’t sign up. This compounding penalty can have a devastating financial impact over a lifetime, turning a manageable premium into a significant financial burden.

The insidious nature of the LEP is how it silently grows. For example, AARP calculations show that a 7-year delay in enrollment results in a 70% permanent premium increase. This can mean paying hundreds of dollars extra each month for the rest of your life for the exact same coverage. This financial drain is especially punishing for those on a fixed retirement income.

What makes this penalty particularly tragic is that it often stems from simple misinformation or lack of awareness. According to the AARP Public Policy Institute, a significant portion of beneficiaries are caught by surprise. As they stated in a report cited by the Medicare Rights Center:

About 20% of people paying the Part B LEP did not know about these penalties at the time they reached age 65

– AARP Public Policy Institute, Medicare Rights Center Report on Late Enrollment Penalties

Avoiding this penalty requires a proactive understanding of enrollment timelines, especially when transitioning from employer-sponsored coverage. If you believe a penalty has been applied in error, you can appeal it, typically by proving you had qualifying health coverage from an employer. However, prevention is far better than the cure, as reversing the penalty is an uphill battle.

When to Switch Plans: The Enrollment Window You Must Not Miss

A common misconception is that you are locked into your health plan for an entire year, forced to wait for the Annual Enrollment Period to make changes. For seniors with worsening chronic conditions, this belief can be dangerously passive. The strategic reality is that Medicare has several lesser-known Special Enrollment Periods (SEPs) that act as powerful « enrollment triggers, » allowing you to switch plans mid-year based on specific life and health events.

Mastering these SEPs is the key to proactive policy restructuring. For instance, if you are diagnosed with a condition that qualifies for a Chronic Condition Special Needs Plan (C-SNP), you are typically granted an SEP to enroll in one of these specialized plans at any time. This is a game-changer, as it allows you to align your coverage with your new diagnosis immediately. Another powerful trigger is a change in residence. Moving into or out of a skilled nursing facility, or even moving to a new location to be closer to a specialist’s hospital, can grant you immediate enrollment rights to choose a new plan that better serves your new circumstances.

These windows are not widely advertised and require you to be an active manager of your own eligibility. Waiting for an annual mailer is a reactive strategy; knowing that a move or a new diagnosis is an enrollment trigger is a proactive one. The table below highlights some of these crucial but often overlooked enrollment windows.

| Enrollment Window | Eligibility | Duration |

|---|---|---|

| Medicare Advantage Open Enrollment | Current MA enrollees only | January 1 – March 31 annually |

| 5-Star SEP | Anyone can switch to 5-star rated plan | December 8 – November 30 (once per year) |

| Chronic Condition SEP | New diagnosis of qualifying condition | Immediate upon diagnosis verification |

| Institution SEP | Moving into/out of nursing facility | While in facility plus 2 months after discharge |

Why Your Insurance Policy Has « Hidden » Prevention Benefits You Never Use?

While most people view health insurance through the lens of covering doctor visits and hospital stays, many modern plans—especially Medicare Advantage plans—contain a wealth of « hidden » benefits designed for prevention and chronic care management. These supplemental benefits are not just minor perks; they are strategic tools that can significantly improve quality of life and reduce out-of-pocket costs. However, they often go unused simply because beneficiaries don’t know they exist or how to access them.

The landscape of these benefits has expanded dramatically. For example, according to AARP’s review of Medicare benefits, since 2020 many Medicare Advantage plans are now permitted to offer special supplemental benefits for the chronically ill. This can include things like grocery allowances, home-delivered meals, funding for home modifications like grab bars, and even pest control. These are not luxuries; they are recognized as essential components of a holistic care plan that keeps seniors safer and healthier at home, preventing more costly hospitalizations down the line.

The key to unlocking this hidden value is the Health Risk Assessment (HRA), a questionnaire your plan sends you annually. Many people rush through these forms, but they are your primary opportunity to signal your needs to the plan. By answering honestly and comprehensively about your functional limitations and health challenges, you can trigger referrals to care managers and unlock eligibility for these supplemental benefits. A care manager can become your internal advocate, navigating the system to connect you with services you didn’t even know you were entitled to. This transforms the HRA from a bureaucratic chore into a strategic request for resources.

Your Action Plan: Uncovering Hidden Plan Benefits

- Identify Contact Points: List all communications from your insurer (HRAs, newsletters, member portals) where benefits might be mentioned.

- Collect Plan Documents: Gather your current plan’s « Evidence of Coverage » and « Annual Notice of Changes » to inventory all listed supplemental benefits.

- Assess for Coherence: Compare the listed benefits against your documented health needs and functional limitations. Do they align?

- Analyze for Value: Create a simple grid to evaluate each potential benefit. Is it a generic wellness program or a tangible benefit like a food allowance or transportation service?

- Execute an Integration Plan: Prioritize the top 2-3 benefits. Contact your plan’s member services to confirm eligibility and the exact steps for activation.

How to Document Medical Necessity to Get Insurance to Pay for Power Chairs?

Securing insurance coverage for a power wheelchair is the ultimate test of the « medical necessity framework. » Insurers like Medicare will not approve such a high-cost item without an ironclad case proving it is the *only* viable option for in-home mobility. To succeed, you must create a clear, logical narrative of escalating need, demonstrating that all lesser forms of mobility aids have been tried and have failed to meet your essential needs. This is often referred to as the hierarchy of mobility documentation.

A successful case meticulously documents this hierarchy. For example, a doctor’s note might state: « Patient used a cane for 6 months, resulting in 3 falls and subsequent ER visits. Patient then progressed to a walker but lacks the upper body strength to ambulate more than 20 feet without severe fatigue. Patient cannot self-propel a manual wheelchair due to severe shoulder arthritis. » This narrative leaves the insurer with only one logical conclusion: the power wheelchair is a medical necessity, not a choice. As Paul Lane of the United Spinal Association’s Tech Access Initiative warns, getting it right the first time is critical:

Medicare won’t pay for that. If you have a chair that doesn’t fit you well and you’re not comfortable in it but Medicare already paid for it, they’re not going to give you another one for five years

– Paul Lane, United Spinal Association’s Tech Access Initiative

The most powerful tool in your documentation arsenal is quantification. Vague statements about difficulty are easily dismissed. Instead, you must translate daily struggles into measurable data related to your Activities of Daily Living (ADLs). This removes all subjectivity and presents your limitations in the clinical, data-driven language that insurers understand and respect. The table below shows how to reframe common problems into powerful, quantified descriptions.

| Vague Description (Often Denied) | Quantified Description (More Likely Approved) |

|---|---|

| Has trouble in kitchen | Unable to safely transport plate from microwave to table (10 feet), creating burn and fall risk |

| Difficulty with bathroom activities | Cannot rise from standard 17-inch toilet without two-person assist, taking 5+ minutes |

| Problems with mobility | Can only ambulate 15 feet with walker before oxygen saturation drops below 88% |

| Needs help with transfers | Requires 2 caregivers and 20 minutes for bed-to-chair transfer, 4 times daily |

Key Takeaways

- Your power lies in proactively documenting medical necessity, not reactively pleading for coverage.

- Special Enrollment Periods (SEPs) are strategic opportunities to switch plans mid-year, triggered by specific health and life events.

- Quantifying your limitations (e.g., « cannot walk more than 15 feet ») is exponentially more powerful than vague descriptions (« has trouble walking »).

How to Organize Complex Medical Records for Seniors Without Getting Overwhelmed?

For any strategic health insurance effort to succeed, it must be built on a foundation of meticulously organized medical records. When you are managing one or more chronic conditions, the sheer volume of paperwork—test results, consultation notes, billing statements, and insurance correspondence—can become completely overwhelming. A shoebox full of papers is not a strategy; it is a liability. An organized system is your single greatest asset, enabling you to quickly retrieve evidence for an appeal, provide a new specialist with a complete history, or prove past coverage to avoid a penalty.

The key to avoiding overwhelm is to stop thinking about a single, monolithic file and instead adopt a multi-part system designed for different purposes. You need a comprehensive archive that stays at home, a nimble « go-bag » for appointments, and a project-specific file when you are tackling a single, major issue like an appeal. This compartmentalization makes the task manageable and ensures you have the right information at the right time, without having to carry a decade’s worth of records to a routine check-up.

The « Three-Binder System » is a proven method for achieving this. It provides a clear, logical structure that you or a caregiver can easily maintain. A crucial element is creating a one-page « Medical Records Cover Sheet » that summarizes your entire health profile—diagnoses, medications, allergies, and provider contacts. This single page becomes the most valuable document in your entire system, providing a high-level overview for any healthcare professional in seconds. Adopting a clear system like the one below transforms record-keeping from a burden into a powerful tool for advocacy.

The Three-Binder System for Medical Record Organization

- Create Master Archive Binder: Keep at home with complete historical records organized by year.

- Assemble Go-Bag Binder: Slim folder with current medication list, provider contacts, insurance cards, and recent test results for all appointments.

- Build Advocacy Binder: A project-specific file for a single appeal or claim, containing all related correspondence and evidence.

- Use Consistent Naming: Adopt a « YYYY-MM-DD_Provider_DocumentType » format for all digital scans to ensure easy retrieval.

- Create a Medical Records Cover Sheet: A one-page summary with diagnoses, medications, and allergies, updated after each significant appointment.

By shifting your mindset from a passive recipient of care to the active, strategic director of your health coverage, you can navigate the complexities of the insurance system. The next logical step is to apply these frameworks to your own situation, beginning with a thorough audit of your current plan’s hidden benefits and your own medical documentation.